The Student Loan Dilemma: Career and Personal Life Consequences

22/11/2023

Jacopo Priori

A collection of points of view about student loans that goes beyond financial implications, to be better informed about their impacts on students’ lives at an individual and a collective level

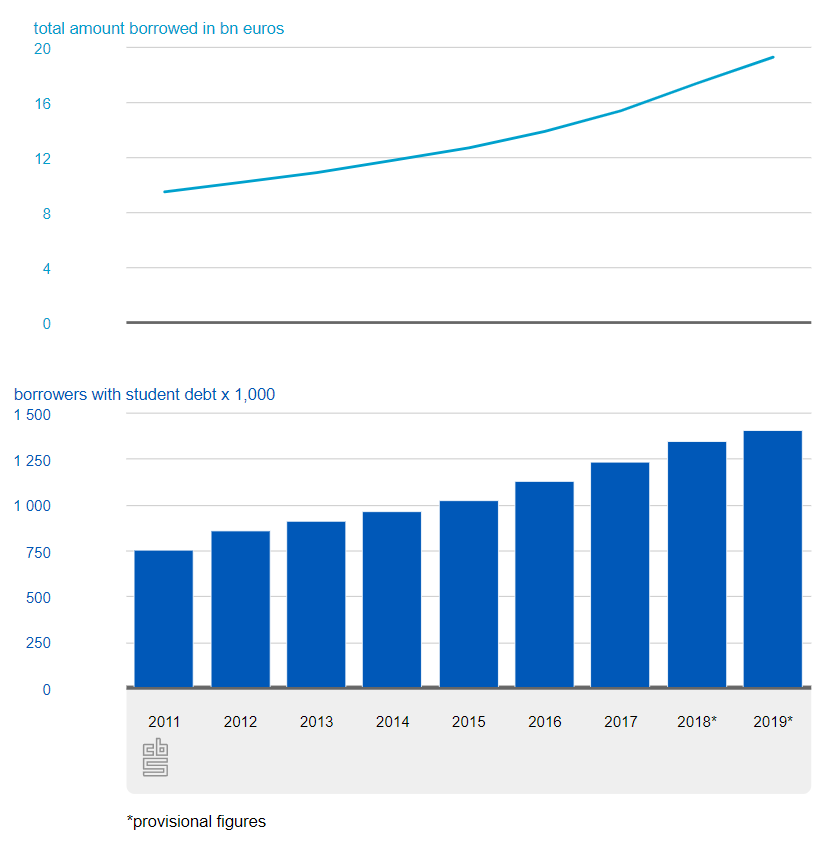

Here in the Netherlands, education is more affordable than in countries such as the US and the UK. Yet, despite government financial incentives and relatively low tuition fees, the topic of student loans is still a significant concern for many. According to CBS, last year the average student debt amounted to €16,400 (CBS, 2023), and the number of borrowers with student debt doubled from 2011 to 2019 (CBS, 2019). The decision to get student loans is crucial, as it can drastically affect one's access to education and future opportunities. While borrowing for education is essential for many students, the consequences of accumulating significant debt cannot be disregarded. This article briefly presents an overview of the complicated landscape of student loans, exploring different points of view and potential implications.

Recently, in the US, the student debt crisis has been intensively debated. A study (Black et al., 2020) analysed the broader impact on human capital and financial welfare. Contrary to fears, higher access to student loans positively correlates with improved degree completion rates and increased loan repayment capacity. Moreover, increased borrowing does not seem to significantly impact other forms of debt. These findings challenge assumptions about the risks linked with student borrowing, suggesting that prudent borrowing can have adverse effects. A similar perspective is given by Barr et al.'s study (2021). An intervention designed to encourage informed borrowing decisions led to reduced loan amounts. However, this reduction resulted in poorer academic performance and a higher incidence of loan defaults. Specifically, a 4% percent lower debt was followed on average by a 3% percent lower GPA, mainly due to higher necessity to spend time on paid work, reducing the amount of study hours. These results highlight the importance of choosing between minimising debt and ensuring educational success, compelling policymakers to consider the consequences of their initiatives.

Getting a degree can leave graduates with large student loans, but it seems like they will make more money and have better chances of obtaining jobs that require a bachelor's degree, according to researchers (Velez et al., 2018). Nevertheless, borrower's decisions about what job to take are usually based on their debt burden. Some may choose higher-paying positions for the short term, which might come at the expense of their long-term career growth, flexibility, and job satisfaction. This crucial trade-off not only determines their professional ambitions but also influences personal life choices, as it is shown that they are less predisposed to marry and start a family, and more likely to have a negative net worth. Psychological well-being and overall health suffer too, confirming the need for a comprehensive life outlook (Kim & Chatterjee, 2018). In particular, a one percent increase in the student loan amount leads to a 1.1% lower probability of life satisfaction and a 1.1% higher probability of reporting psychological problems. Furthermore, home ownership is significantly delayed (Mezza et al., 2020).

Besides these individual-level implications, policies play a fundamental role in managing student loans. Governments and educational institutions worldwide struggle to find an equilibrium between ensuring access to education and avoiding a worrying debt crisis. Balancing financial aid structures, interest rates, and loan repayment options remains challenging. An interesting remark on the policy framework comes from Zhang's study (2019), which evaluates the impact of varying debt levels on spending behaviours. Individuals with huge debt tend to spend more, driven by the perceived challenge of repaying a significant amount. It is then suggested that presenting debt in small monthly instalments can partially prevent this harmful behaviour since students perceive the debt amount as easier to repay.

The current debate surrounding student loans is indeed quite controversial. The decision to borrow for education must be evaluated carefully, considering potential trade-offs between immediate gains and long-term consequences. For students, informed decision-making regarding student loans remains critical as they make this complex choice that shapes their academic and professional careers.

References

-

Barr, A., Bird, K., & Castleman, B. (2021). The effect of reduced student loan borrowing on academic performance and default: Evidence from a loan counseling experiment. Journal of Public Economics, 202, 104493.

-

Black, S. E., Denning, J. T., Dettling, L., Goodman, S., & Turner, L. J. (2020). Taking it to the limit: Effects of increased student loan availability on attainment, earnings, and Financial Well-Being. National Bureau of Economic Research Working Paper Series, 27658.

-

CBS. (2023). How many people have a student debt? - The Netherlands in Numbers.

-

CBS. (2019). More students taking out higher student loans.

-

Kim, J., & Chatterjee, S. (2018). Student Loans, Health, and Life Satisfaction of US Households: Evidence from a Panel Study. Journal of Family and Economic Issues, 40(1), 36–50.

-

Mezza, A., Ringo, D., Sherlund, S. M., & Sommer, K. (2020). Student loans and homeownership. Journal of Labor Economics, 38(1), 215–260.

-

Velez, E. D., Cominole, M., & Bentz, A. (2018). Debt burden after college: the effect of student loan debt on graduates’ employment, additional schooling, family formation, and home ownership. Education Economics, 27(2), 186–206.

-

Zhang, Y., Wilcox, R. T., & Cheema, A. (2019). The Effect of student loan debt on spending: The role of repayment format. Journal of Public Policy & Marketing, 39(3), 305–318.